What operators need to know heading into leasing season 2026.

SCOTTSDALE, AZ — When multifamily leaders want to understand where the rental housing market is headed next, they turn to Jay Parsons.

A nationally recognized housing economist, Parsons spent years helping investors, developers, lenders, and operators make sense of the forces shaping rental housing. Prior to launching his advisory work, he served as Chief Economist at RealPage, where he analyzed housing trends and market performance across the country. Today, Parsons works as a consultant, speaker, and podcast host, translating complex housing data into insights the industry can act on.

At Forum, Parsons framed today’s multifamily environment as a mix of short-term pressure and long-term confidence. Operators are feeling real strain from investors as returns lag expectations, and uncertainty remains a constant backdrop. But structurally, the fundamentals of rental housing are still strong, driven by a highly competitive and fragmented industry where operators of all sizes can compete and win.

Parsons focused on eight key forces impacting multifamily, all pointing to a supply-driven reset rather than a broken demand story.

“I know you remember, survive until ‘25, and now there’s a fix in ‘26, it’ll be heaven in ‘27, it’ll be great in ‘28,” Parsons said. “We’ll keep coming up with new ones until one day it’s right. I don’t know if it’s going to fix in ‘26, but I do think we’re going to see some improvement this year.”

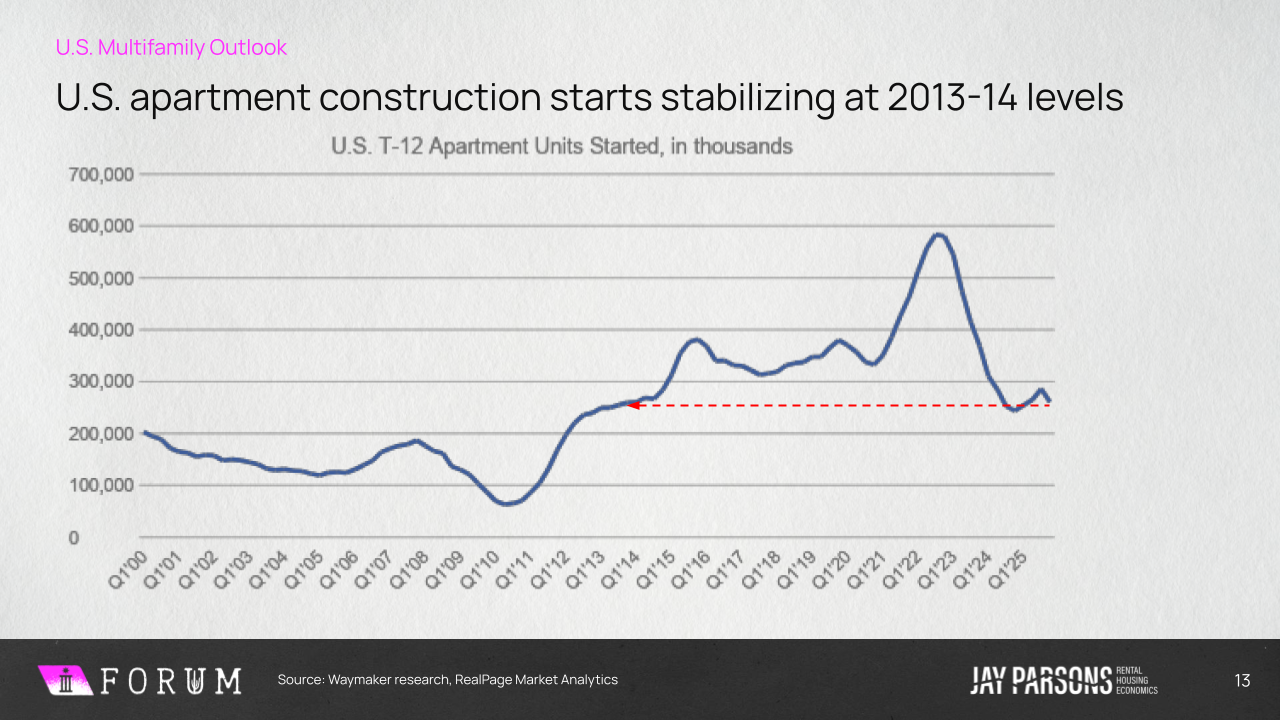

1. One thing we do know: Apartment supply WILL drop substantially in 2026

Parsons level-set the conversations with two important notes about the current state of multifamily:

- Everything is cyclical.

- The long-term tailwinds around multifamily are really strong.

One of the most prominent cyclical patterns multifamily is facing right now is the tug-of-war between supply and demand, which Parsons says is one of the largest contributors to today’s tough market.

“There’s a lot of uncertainty right now, but one thing we do know is this: There’s going to be less supply this year,” Parsons said. “Supply is an easy thing to forecast. I can’t tell you with great certainty what’s going to happen with demand this year. There’s going to be a lot of variables that we might take on, but supply we know is going down.”

After peaking at historic highs in 2024, the pipeline is finally contracting back to 2013-14 levels.

“We’re at the point where those numbers really do drop off. And in these next few years, we will be seeing supply levels that are around 10-year lows,” Parsons said.

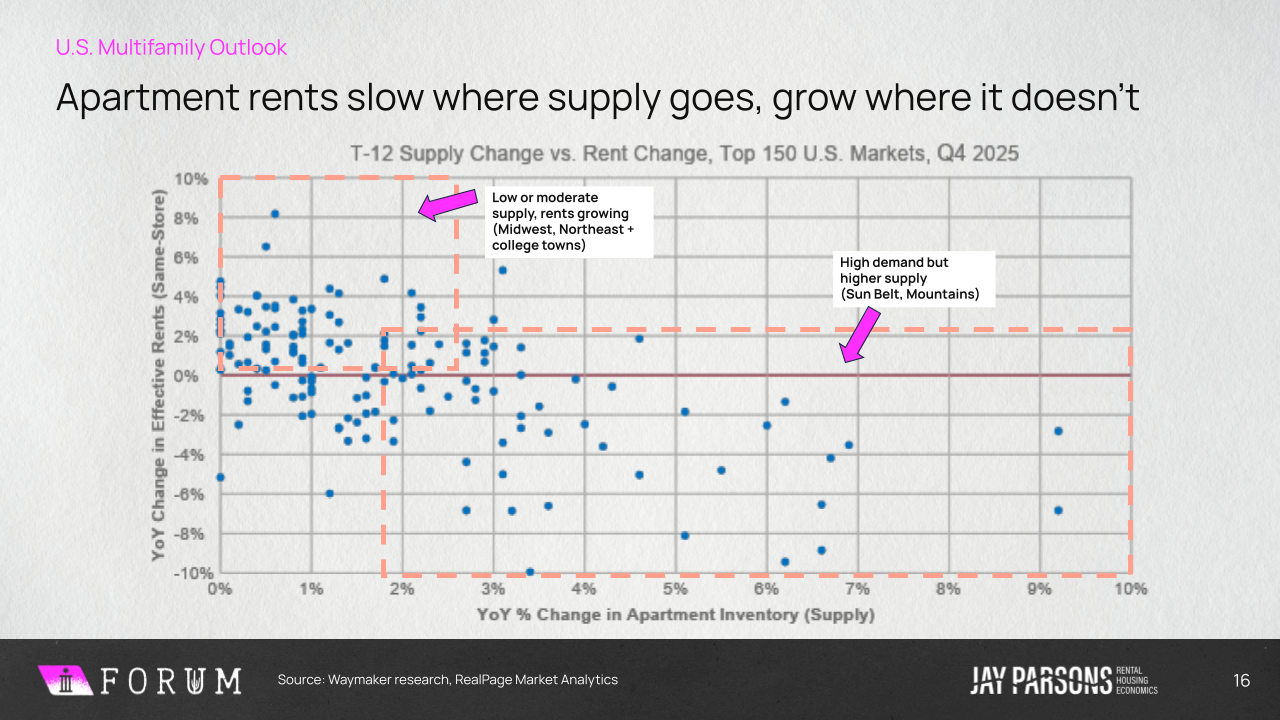

2. Rent filtering continues to play out as supply wave pushes down market-rate rents

If supply is the root cause, the downstream effects are showing up everywhere.

From Class A to Class C, rent movement today isn’t being driven by weakening demand, but by how much new inventory each market is absorbing.

“It’s still all about supply,” Parsons said. “Supply is the number one, number two, and number three factor.”

In high-supply markets, operators are seeing rents decline even as demand remains strong. In fact, many of the markets cutting rents are actually absorbing more units than those seeing rent growth.

What’s happening is a ripple effect. As new Class A units are delivered, higher-income renters move up. That opens space in Class B. Which then puts pressure on Class C.

“The markets that are cutting rents have far more demand than the markets that are raising rents… so it’s not a demand issue. It’s a supply issue,” Parsons said.

Even affordable and workforce housing aren’t immune. As filtering continues, rent pressure is cascading further down the stack than many expected.

3. Maybe it’s not “It’ll Fix in ‘26,” … but 2026 SHOULD bring some improvement

After a volatile 2025, the question isn’t whether things will improve, it’s how much.

Parsons pushed back on the industry’s tendency to overcorrect with overly optimistic timelines.

“I don’t know if it’s gonna fix in ‘26,” he said. “But I do think we’re going to see some improvement this year.”

Across most markets, rent declines are slowing. Seasonal patterns are starting to normalize. And while growth hasn’t fully returned, momentum has shifted.

“What we’re seeing… is not a massive rebound, but it started to get a little bit better,” Parsons said.

That distinction matters. Operators shouldn’t expect a snap-back year. But they also aren’t operating in the same environment as 2025.

The recovery is happening, just more gradually than anyone would prefer.

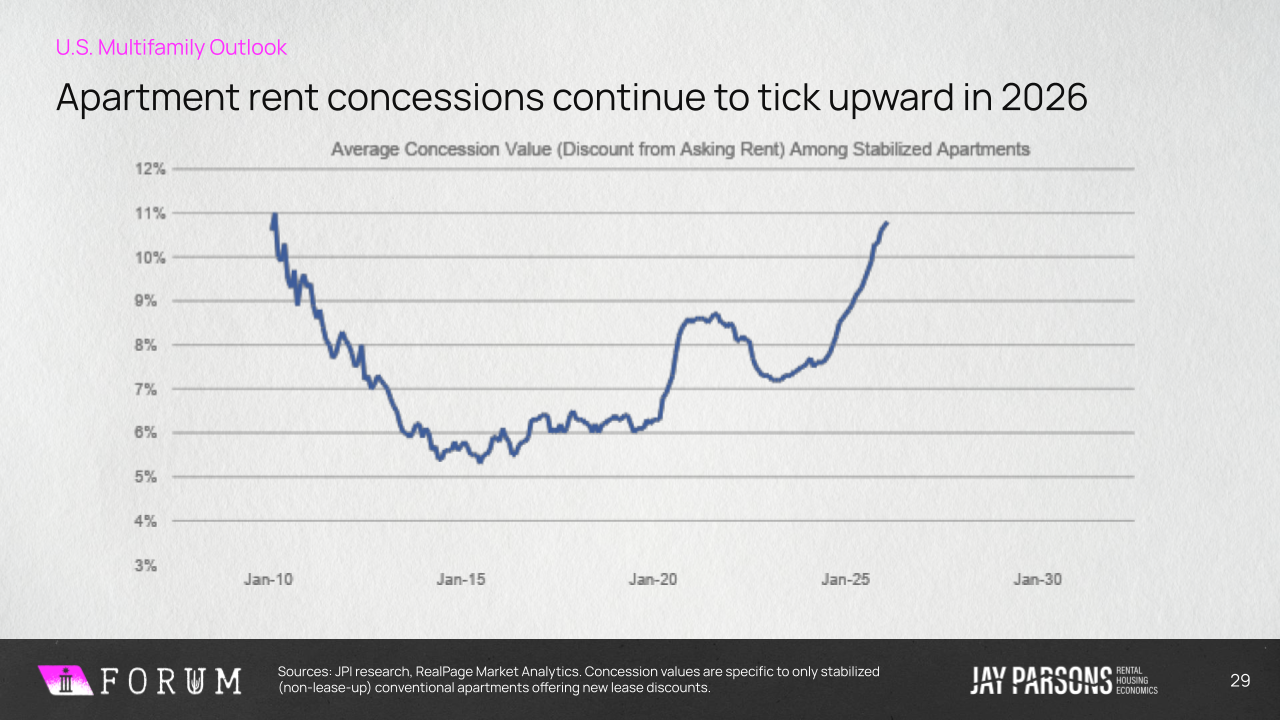

4. Lease-ups remain challenged for rent growth, further limiting new starts

Even as supply begins to pull back, the industry is still working through the backlog of deliveries from the last two years.

“We still have a lot of units that are still in lease-up,” Parsons said. “It’s hard to absorb that much supply overnight.”

In many high-supply markets, lease-ups are competing aggressively on price, pushing rents down just to maintain occupancy.

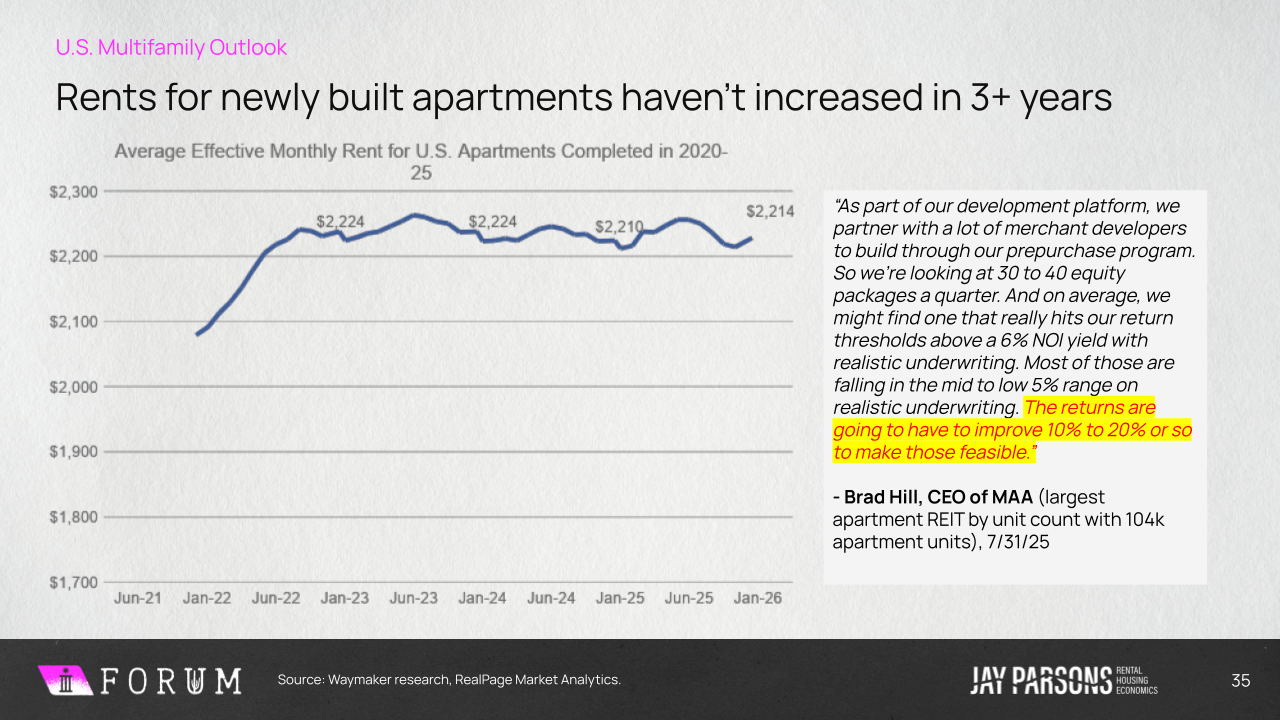

At the same time, rents for newly built assets are flat, and have been for years, while development costs continue to rise. That disconnect is making it increasingly difficult for new deals to pencil.

“They’re building to the number from three years ago. That makes it really tough.”

The result is a natural slowdown in new starts, reinforcing the supply reset already underway.

Parsons also pointed out that renters are increasingly looking for a deal on their rent. Much like you don’t take the MSRP when buying a car, Parsons says, renters are conditioned to expect some concession.

“In some of these markets, I think we’ve conditioned renters into some of the same thinking,” Parsons said. “They have great income, it’s not about affordability, but they’ve heard everyone is getting a deal, so they want one too.

“I’m curious how this will play out. I think you’ll see concessions in some market sticks, not because demand is weak or vacancy issues, but we’ve conditioned renters to expect it. This is theoretical, but we could see a situation where, kind of like with car dealers, we raise the concession and raise the asking rent to sort of preserve the psychology of the deal.”

5. Absorption will likely drop off in 2026, and yet … vacancy still improves

Absorption is one of the most misunderstood metrics in multifamily, especially in a cycle like this.

At its core, absorption is simple: it’s the net number of units that go from vacant to occupied over a given period.

But here’s the nuance Parsons emphasized, absorption isn’t just a measure of demand. It’s also constrained by supply.

“You can only absorb what is available,” he said. “As supply goes down, absorption is going to go down because absorption capacity is going down.”

That means a drop in absorption in 2026 isn’t necessarily a red flag. It may just reflect the fact that there are fewer new units hitting the market to be filled.

What actually matters is the relationship between supply and absorption.

If absorption declines faster than supply, vacancy rises and that signals a real demand problem. But if absorption continues to outpace new deliveries, even at lower levels, vacancy can still improve.

And right now, the data is pointing in that direction.

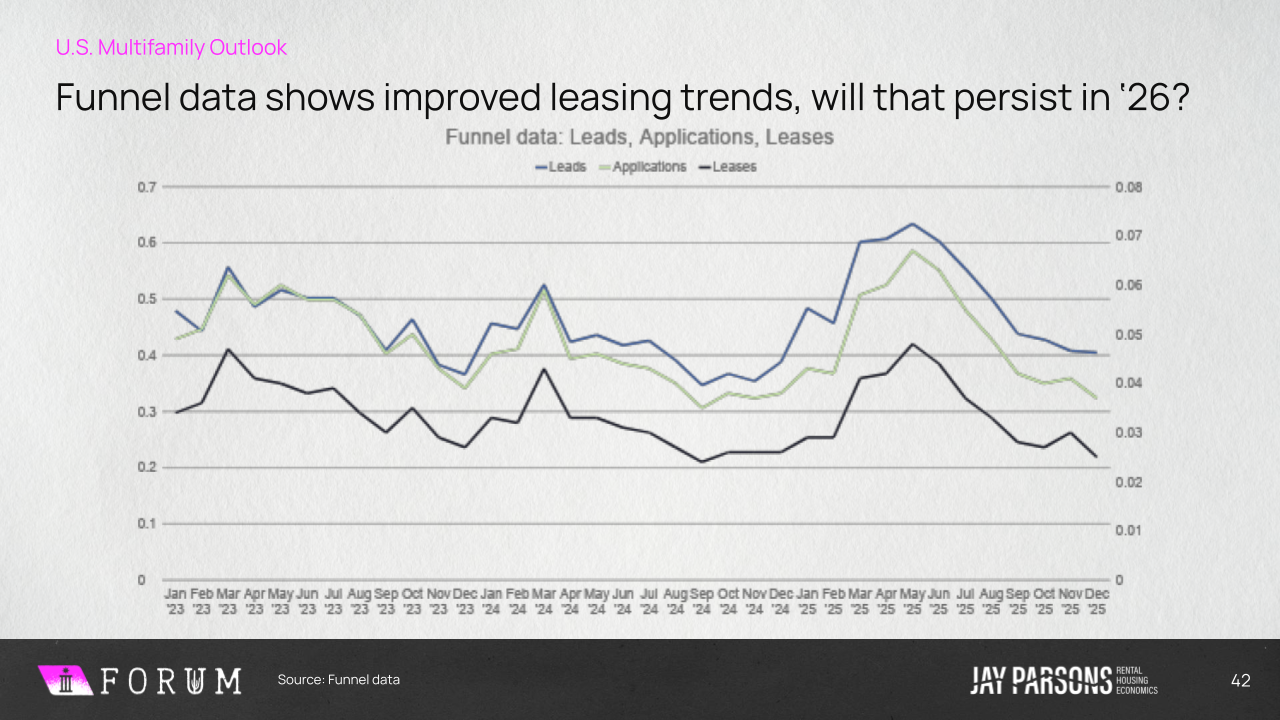

Anonymized, aggregate data from Funnel shows leasing activity trending up over the past year, with a noticeably stronger peak during the 2025 leasing season compared to 2023 and 2024. Leads, applications, and leases are all moving in the right direction, and lead-to-lease velocity continues to improve.

“We have seen some improvement in lease activity over the last 9 months or so, with the lead volume and lease volume is incrementally getting better,” Parsons said. “The velocity has really improved for those using Funnel with the time between lead to lease [shrinking]. That reflects the software as well as a good execution. And to see the lead-to–lease materially shrink down since 2023, which is a good sign as well.

“It’s gradually getting better, which I think is the general trajectory of this whole recovery,” Parsons said.

6. Immigration policy impacts will likely be isolated, not systemic across rental housing

Parsons suggested Immigration impact on multifamily performance is limited at a macro level. When impacts do occur, they tend to be highly localized.

The broader takeaway: immigration may create short-term disruption in pockets of the market, but it is not a systemic driver of occupancy or rent performance across multifamily.

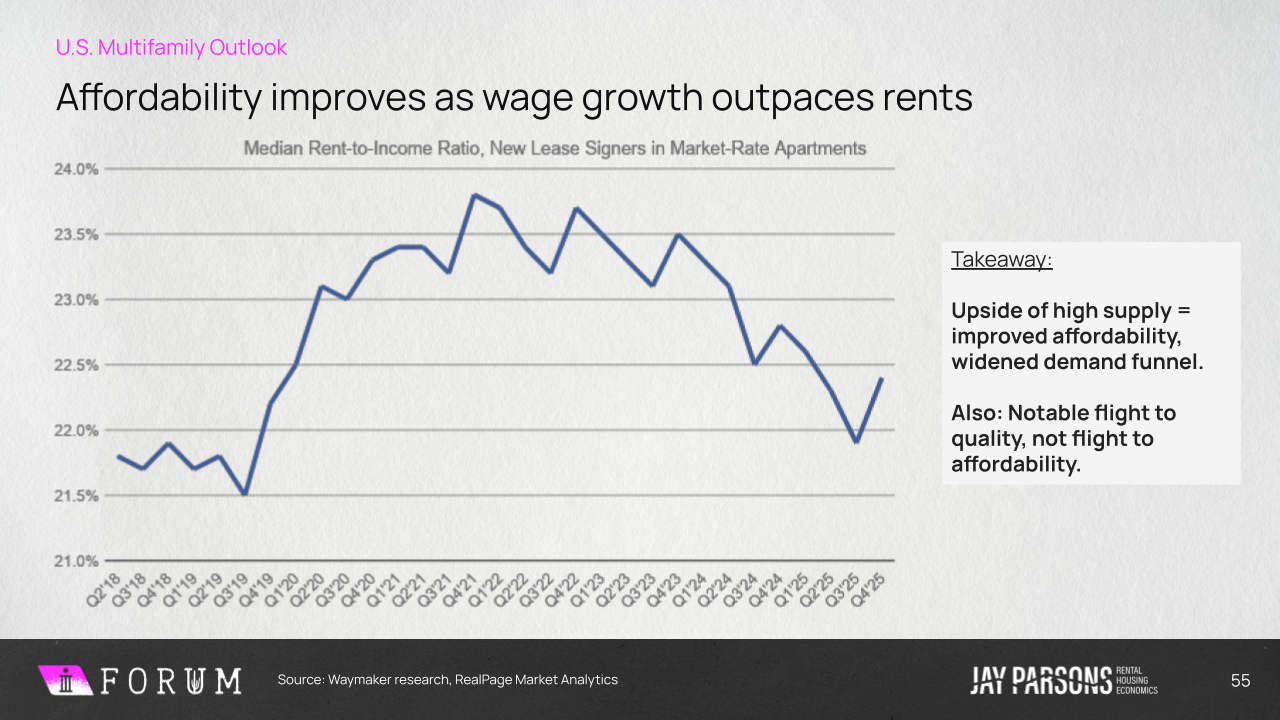

7. Rent affordability will likely continue to IMPROVE despite headline narratives.

One of the more surprising takeaways from Parsons’ analysis is that affordability is quietly trending in the right direction.

“We’ve had three straight years of rent growth that’s been slower than wage growth,” he said. “That’s a good thing.”

As wages continue to outpace rent increases, many renters are regaining financial flexibility.

Rent-to-income ratios have normalized closer to pre-COVID levels, particularly for middle- and higher-income renters.

At the same time, Parsons acknowledged the nuance in the data.

Affordability challenges haven’t disappeared, they’ve become more concentrated.

Lower-income renters continue to feel pressure, while those earning above $50K are generally in a much more stable position.

The takeaway: affordability isn’t universally improving, but the overall trend is moving in a healthier direction than headlines suggest.

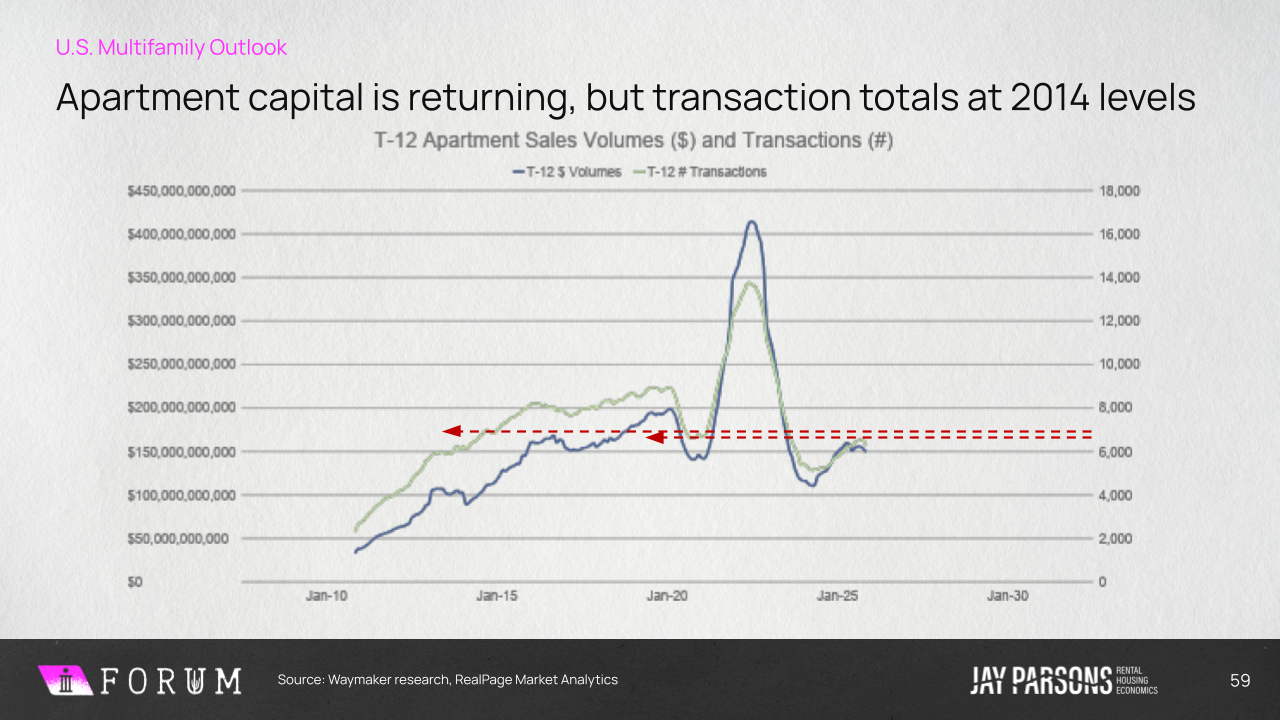

8. Apartment sales volumes will moderately pick up, and investors are much more focused on stronger submarkets, not just in metro areas.

Transaction volume remains below historical norms, but capital is starting to re-enter the market with a more selective lens.

“We’re at the lowest levels since 2014,” Parsons said. Investors aren’t returning evenly across markets. Instead, they’re targeting specific submarkets with stronger fundamentals.

“In these higher-rent submarkets… capital is coming back faster than in these cheaper areas.”

Rather than broad MSA bets, capital is concentrating in neighborhoods with better rent profiles, newer assets, and more resilient demand.

That shift reflects a more disciplined investment environment, one where precision matters more than scale.

Short-term pressure. Long-term confidence.

If there was one theme that carried through Parsons’ keynote, it’s this: multifamily is operating in a moment of short-term pressure and long-term confidence.

Operators are feeling it from all sides. Investor expectations haven’t reset as quickly as market conditions. Lease-ups are competitive. And uncertainty still lingers across markets.

But zoom out, and the fundamentals haven’t changed.

As Parsons reminded the room, “everything is cyclical.” And what we’re seeing now is a supply-driven cycle beginning to turn. The same forces creating pressure today in record deliveries, aggressive concessions, pricing resets, and they are already starting to unwind.

Underneath it all, the structure of rental housing remains intact: a highly competitive, deeply fragmented industry where operators of all sizes can compete and win.